When it comes to tax policies, few figures in American politics have been as polarizing as Donald Trump. His approach to taxation, particularly concerning the wealthy, has sparked intense debates across the political spectrum. As discussions around fiscal responsibility and economic growth continue, understanding Trump's stance on taxing the rich becomes crucial. This article delves into why Trump opposes tax hikes on the wealthy, exploring the reasoning behind his position and its implications for the broader economy.

In recent years, the discourse surrounding wealth distribution and taxation has intensified, with various proposals aiming to increase taxes on the rich gaining traction. However, Trump remains steadfast in his opposition to such measures. His rationale is rooted in beliefs about economic stimulation, job creation, and maintaining incentives for investment. By examining key arguments both supporting and challenging his viewpoint, we can better understand the complexities of this issue and its potential impact on different segments of society.

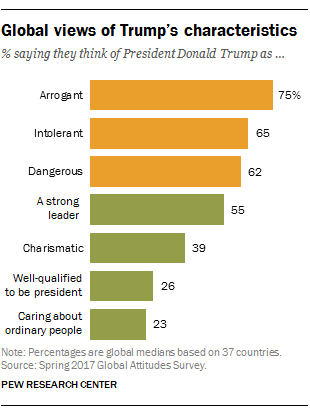

Tax Cuts vs. Tax Hikes: The Divide Between Harris and Trump

Under Trump's plans, individuals in the top 0.1% of earners could see a significant boost in their post-tax income, averaging an additional $376,910. Conversely, the poorest 20% would experience only minimal gains. This disparity highlights the fundamental differences between Trump's approach and that of Vice President Kamala Harris, who advocates for increased taxation on the wealthy to fund public services and reduce inequality. Trump argues that substantial tax cuts will stimulate economic growth, creating a ripple effect that benefits all Americans.

Proponents of Trump's strategy believe that lower taxes on the rich encourage reinvestment into businesses, leading to job creation and innovation. They contend that when high-income individuals retain more of their earnings, they are more likely to invest in ventures that drive economic expansion. Critics, however, argue that such policies primarily benefit the affluent, exacerbating income disparities and placing undue financial burdens on middle- and low-income families.

As the debate unfolds, policymakers must weigh these competing perspectives to determine the most effective path forward. Balancing fiscal responsibility with equitable wealth distribution remains a central challenge in crafting tax legislation that serves the interests of all citizens.

Reevaluating Commitment to Tax Cuts for the Wealthy

Recent developments within the Republican Party suggest a reconsideration of their traditional commitment to tax cuts for the wealthy. In light of the Trump agenda bill, some GOP lawmakers are exploring the possibility of implementing a tax hike on the wealthy to address budgetary concerns. This shift reflects evolving priorities within the party as it seeks to align its fiscal policies with changing voter demographics and economic realities.

The unexpected emergence of this debate underscores the complexity of navigating modern political landscapes. As Republicans grapple with how best to finance their ambitious budget proposals, they face mounting pressure to justify any increases in taxation. Proponents of raising taxes on the wealthy emphasize the need for revenue generation to support essential programs and infrastructure projects, while opponents warn of potential negative consequences for economic growth.

This internal dialogue within the GOP highlights the ongoing tension between ideological principles and practical considerations. Moving forward, finding common ground amidst these divergent views will be critical in shaping future tax policy decisions.

Analyzing the Economic Impact of Trump's Tax Proposals

According to estimates from the Tax Foundation's General Equilibrium Model, Trump's proposed tax cuts could yield significant long-term economic benefits. However, these gains might be partially offset by the adverse effects of tariffs and retaliatory measures from trading partners. Understanding the interplay between these factors is essential in assessing the overall effectiveness of Trump's tax plan.

Supporters of the plan argue that reducing tax burdens on corporations and high-income individuals fosters an environment conducive to business expansion and job creation. They assert that such measures incentivize innovation and productivity, ultimately contributing to sustained economic prosperity. Meanwhile, detractors caution against prioritizing short-term gains over long-term stability, emphasizing the importance of equitable wealth distribution and social welfare investments.

Evaluating the trade-offs inherent in Trump's tax proposals requires careful consideration of both theoretical projections and real-world outcomes. Policymakers must strive to balance economic growth objectives with societal needs, ensuring that tax reforms enhance rather than hinder opportunities for all Americans.

Preventing Tax Hikes Through Budget Resolutions

House Majority Leader Steve Scalise emphasized the importance of passing the House budget resolution to prevent tax hikes on Americans. In line with President Trump's agenda, this resolution aims to secure the border, promote energy production, stimulate economic growth, and reduce government waste. By laying the groundwork for these initiatives, lawmakers hope to safeguard against undue financial burdens on middle-class families and small business owners.

Scalise highlighted the significance of preserving Trump's no-tax-on-tips promise, underscoring the administration's commitment to protecting vulnerable populations from regressive tax policies. Advocates of this approach stress the necessity of fostering an economic climate where all citizens can thrive without fear of excessive taxation. Opponents, however, question whether such measures adequately address systemic inequalities and resource allocation challenges.

As legislative discussions progress, striking a balance between fiscal discipline and progressive reform will remain paramount. Ensuring that budget resolutions reflect the diverse needs and aspirations of the American populace will be key to achieving sustainable economic success.

Addressing Unrealized Capital Gains Taxation

Arguments against taxing unrealized capital gains of the very wealthy often center around existing mechanisms already in place for middle-income households. For instance, property taxes typically rise alongside home values, imposing recurring financial obligations on homeowners regardless of realized profits. Similarly, certain asset classes owned by middle-income families are subject to taxation structures akin to those proposed for unrealized gains.

Opponents of expanded unrealized capital gains taxation argue that extending such practices to wealthier individuals may not yield anticipated revenues while potentially discouraging investment activities. They contend that maintaining current frameworks ensures fairness and consistency across socioeconomic groups, minimizing disruptions to established financial systems. Proponents, however, maintain that targeted adjustments could generate much-needed funds for critical public services and infrastructure improvements.

Navigating this contentious issue demands thorough analysis of existing tax structures and their implications for various stakeholders. Crafting equitable solutions that account for differing perspectives will be vital in advancing comprehensive tax reform efforts.

Evaluating the Distributional Effects of Trump's Tax Plan

A distributional analysis conducted by the Institute on Taxation and Economic Policy reveals that Trump's tax proposals would predominantly benefit the richest 5% of Americans, resulting in tax cuts for this group while increasing taxes for all other income brackets. Such findings raise important questions about the fairness and inclusivity of the proposed measures. Supporters argue that concentrating tax relief among higher earners stimulates economic activity, benefiting society at large through trickle-down effects.

Critics counter that concentrating wealth in fewer hands perpetuates inequality and undermines opportunities for upward mobility among lower- and middle-income households. They advocate for alternative approaches that prioritize broad-based tax reductions, ensuring that financial relief reaches those most in need. Addressing these concerns necessitates thoughtful deliberation and collaboration among policymakers, economists, and community leaders.

Moving forward, achieving consensus on tax policy directions will require addressing underlying issues related to wealth distribution, economic opportunity, and social justice. By engaging in constructive dialogue and embracing innovative solutions, stakeholders can work towards crafting tax reforms that foster inclusive growth and shared prosperity.